How indexing unemployment can restore state trust funds, cut taxes, and grow the workforce in the wake of COVID-19

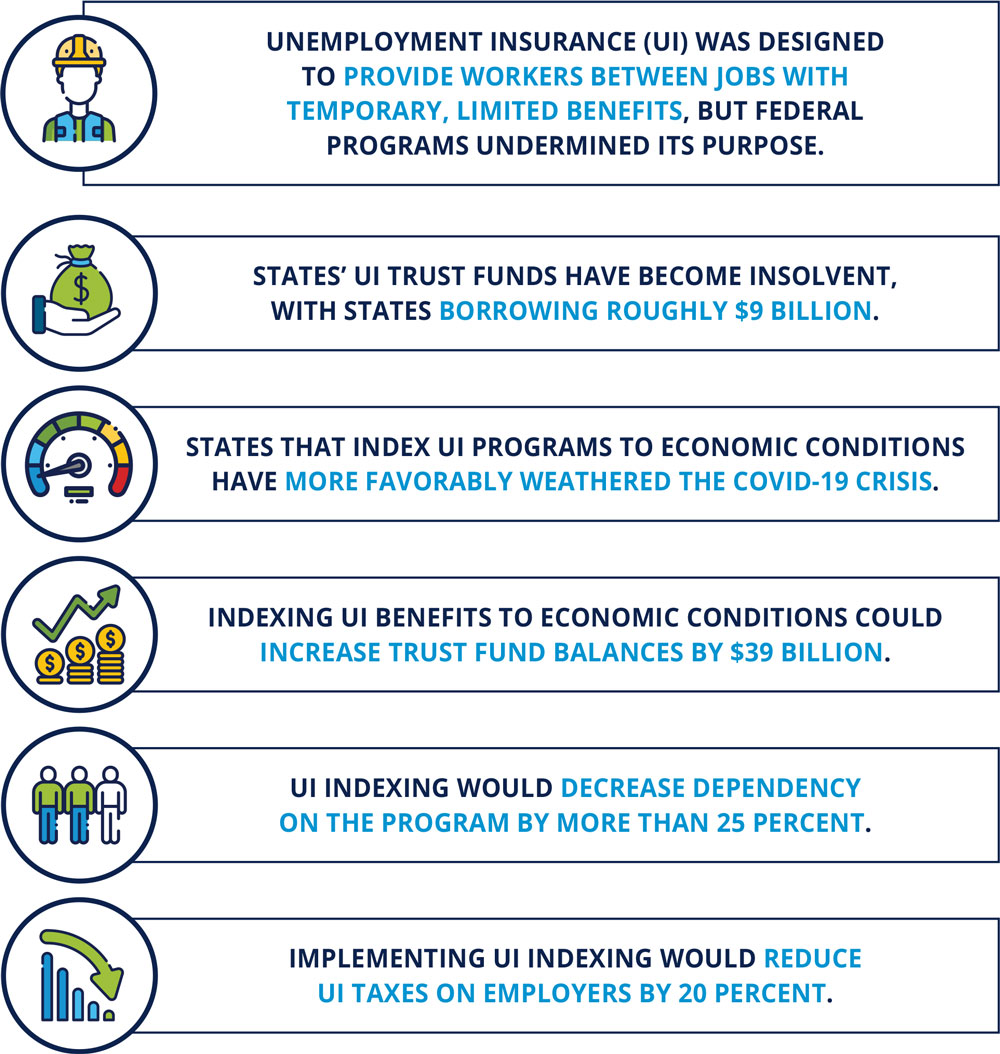

KEY FINDINGS

THE BOTTOM LINE:

States should bolster UI trust funds, cut taxes for small businesses, and move the unemployed back to work by indexing UI benefits to economic conditions.

Overview

Unemployment insurance was designed to provide temporary, limited benefits to assist unemployed individuals while they searched for work. However, the entire concept of UI was turned upside down by COVID-19 and Congress’s response to it. By implementing a $600 weekly UI bonus in the CARES Act, Congress discouraged work and opened the floodgates to fraud.1 Although the unemployment bonus in the CARES Act expired, Congress resurrected and extended additional bonuses—including in President Biden’s so-called American Rescue Plan Act—which continued the harmful impact caused by the original boost.2–3–4–5 Even though the $300 weekly bonus has expired, states’ UI trust fund balances have plummeted—leaving them in dire straits.

UI systems buckled under COVID-19 “relief” schemes

The $600 weekly unemployment bonus Congress passed in 2020 nearly tripled unemployment benefits, with average payouts equivalent to $50,000 per year.6 More than two-thirds of unemployed individuals were receiving more in benefits than they would have earned working.7 This bonus was followed by a similarly disastrous $300 weekly bonus that did not expire nationally until September 2021.8–9 As a result, states’ trust fund balances have plummeted.

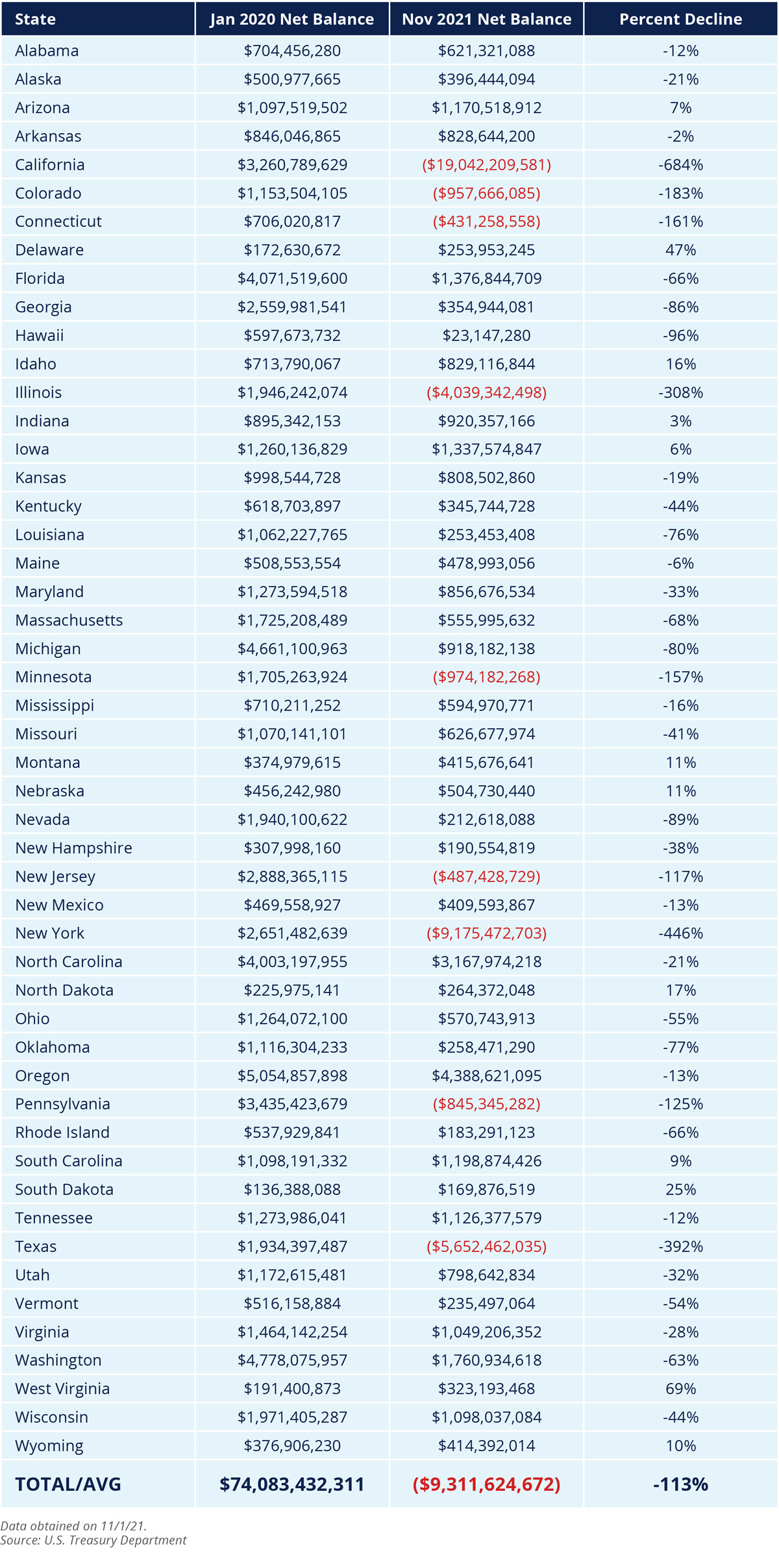

In January 2020, states had nearly $75 billion saved in their UI trust funds to weather the next economic downturn.10 But by November 2021, those trust funds were more than $9 billion in the red.11 State UI trust funds declined by 113 percent on average over this time period.12 The duration of unemployment claims also increased, resulting in higher unemployment taxes paid by businesses.13 As a result, many states’ trust funds have become completely insolvent, forcing them to borrow from federal taxpayers just to pay out weekly benefits and risk future tax hikes.14

This massive drawdown was caused by a number of factors, including the spike in unemployment claims from lockdowns, federal programs that discouraged work, and a nationwide increase in unemployment fraud.

Larger UI payments encouraged fraud

As businesses tried to reopen, they faced a new challenge: getting workers to come back.15 Jennine and Dave Dayler, owners of Saloon on Calhoun with Bacon in Brookfield, Wisconsin, characterized the typical response they got as: “We’re really sorry, but we’re making more on unemployment.”16 Small businesses struggled to compete with unemployment benefits, despite the fact that laid off workers refusing suitable job offers are committing unemployment fraud.17

In part because of how attractive the unemployment bonus—and its later resurrections—made attempting fraud, other high-profile examples occurred, including an amateur rapper allegedly stealing $1.2 million in benefits, state officeholders’ names being used to file claims, judicial employees allegedly committing fraud, and prisoners receiving benefits from behind bars.18 The bonus even made it profitable for international crime rings to attack state unemployment systems, including one stealing hundreds of millions of dollars from Washington state.19 All told, estimates suggests total improper payments to be above $300 billion.20 For comparison, this is more than 100 times greater than the estimated unemployment improper payments in 2019.21

Well-designed unemployment systems do not try to become cradle-to-grave welfare programs. Instead, the best unemployment programs operate on a fundamental premise: Unemployment is about reemployment.

Indexing states weathered COVID-19 better than non-reform states

States were facing similar issues during the Great Recession. Congress extended how long people could remain on unemployment, UI trust funds went insolvent, and states borrowed billions from federal taxpayers just to keep paying out benefits.22 In 2011, Florida addressed these challenges by creating an innovative new structure for the state’s benefits to more closely match job availability.23 Over the next two years, Georgia and North Carolina followed suit.24 In all three states, the length of time that individuals may collect benefits is tied to economic conditions.25 When the unemployment rate is high, individuals have longer to find work. When unemployment is low—and open jobs are high—individuals cycle out of the program sooner.

The results for these indexing states have been dramatic. Prior to COVID-19, indexing states had superior results relating to UI tax rates, program duration, and trust fund balances compared to their non-reform counterparts.26

However, even more impressive than their pre-pandemic performance, indexing states have weathered the COVID-19 crisis far more favorably than non-reform states which allow claimants to remain on the program for 26 weeks. As of November 2021, indexing states’ UI trust funds are in the black, while non-reform states are more than $14 billion in the red.27-28 Notably, no states had insolvent unemployment trust funds in January 2020, demonstrating how quickly states with outdated unemployment benefit structures can find themselves in bad fiscal positions, leading to borrowing and tax increases.29

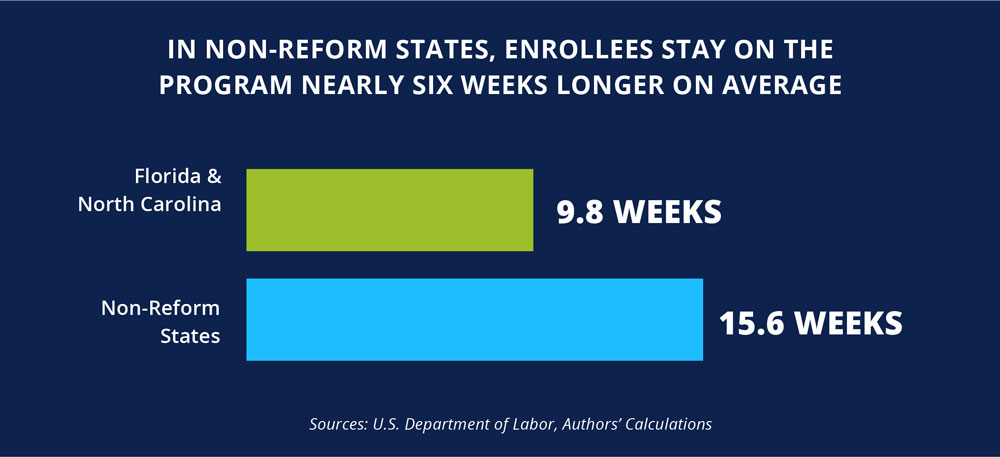

Indexing states also cycle people off of unemployment more quickly, resulting in lower UI taxes on employers.30 In fact, the average UI enrollee in reform states cycles off of unemployment in 9.8 weeks.31-32 In non-reform states, enrollees stay on the program nearly six weeks longer on average.33 Moving individuals from unemployment to work means lower costs, translating into lower taxes on employers. Employers in reform states pay approximately $1.90 in UI taxes for every $1,000 in payroll.34 But businesses in non-reform states pay more than three times that, with employers paying an average of roughly $4.80 for every $1,000 in payroll.35

The culture put in place by emphasizing reemployment has paid off for indexing states. When other states will be contemplating unemployment tax increases, indexing states will remain among the nation’s most economically competitive in that area.

States that index now will be better off

Case studies of Florida, Georgia, and North Carolina demonstrate that indexing states outperform their 26-week counterparts in every important metric. However, opportunity remains for non-reform states to join their indexing counterparts.

If all states indexed their unemployment systems to economic conditions and experienced similar results to those in Florida, Georgia, and North Carolina, they would be able to replenish their trust funds, move individuals off of unemployment more quickly, and reduce taxes on small businesses.

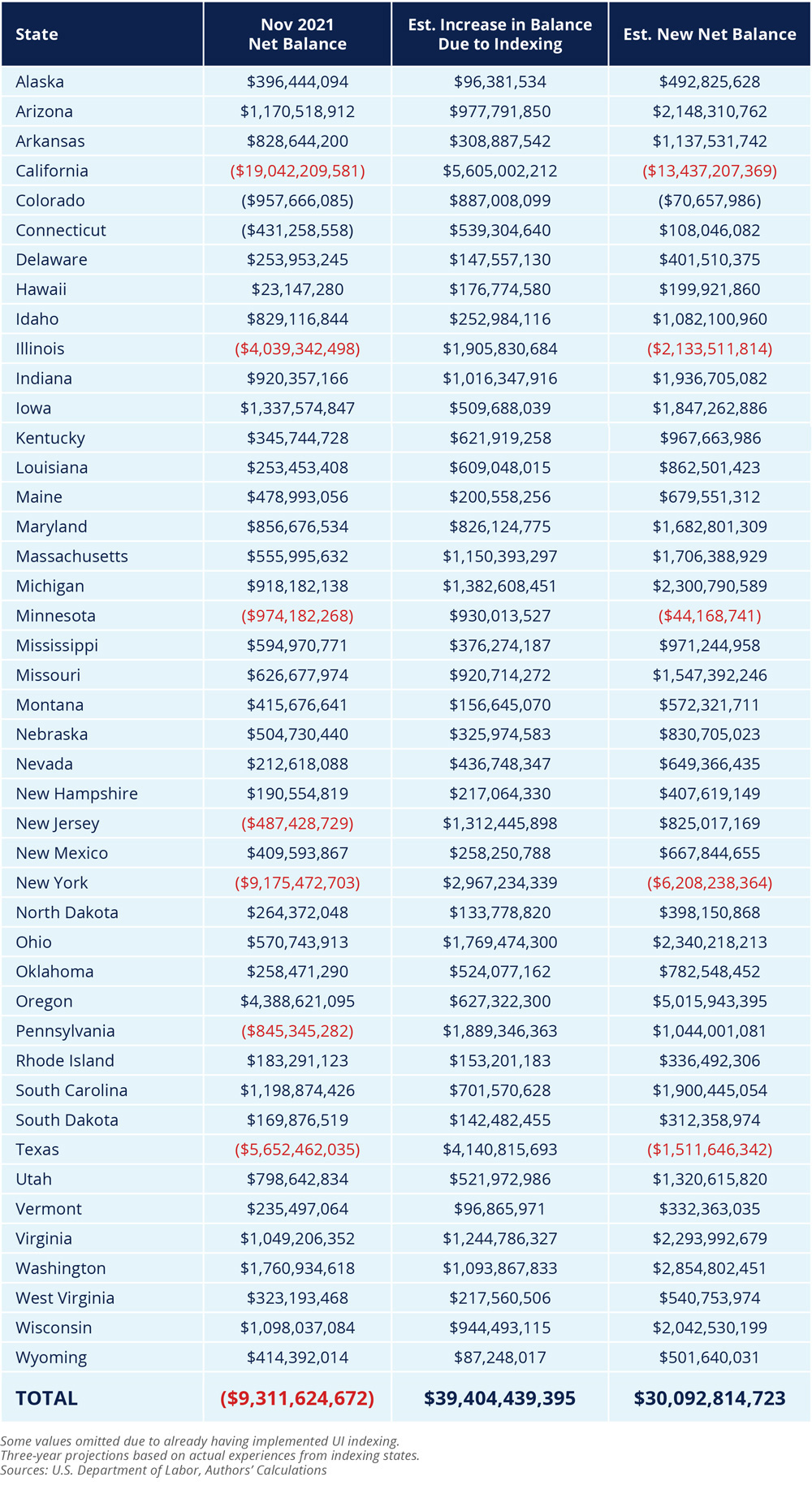

In fact, within three years, state unemployment trust funds would increase to nearly $30 billion in the black compared to the current level of more than $9 billion in the negative—a $39 billion swing.36 This is caused in large part by the average unemployed worker leaving the program 4.6 weeks sooner, or more than 25 percent faster.37

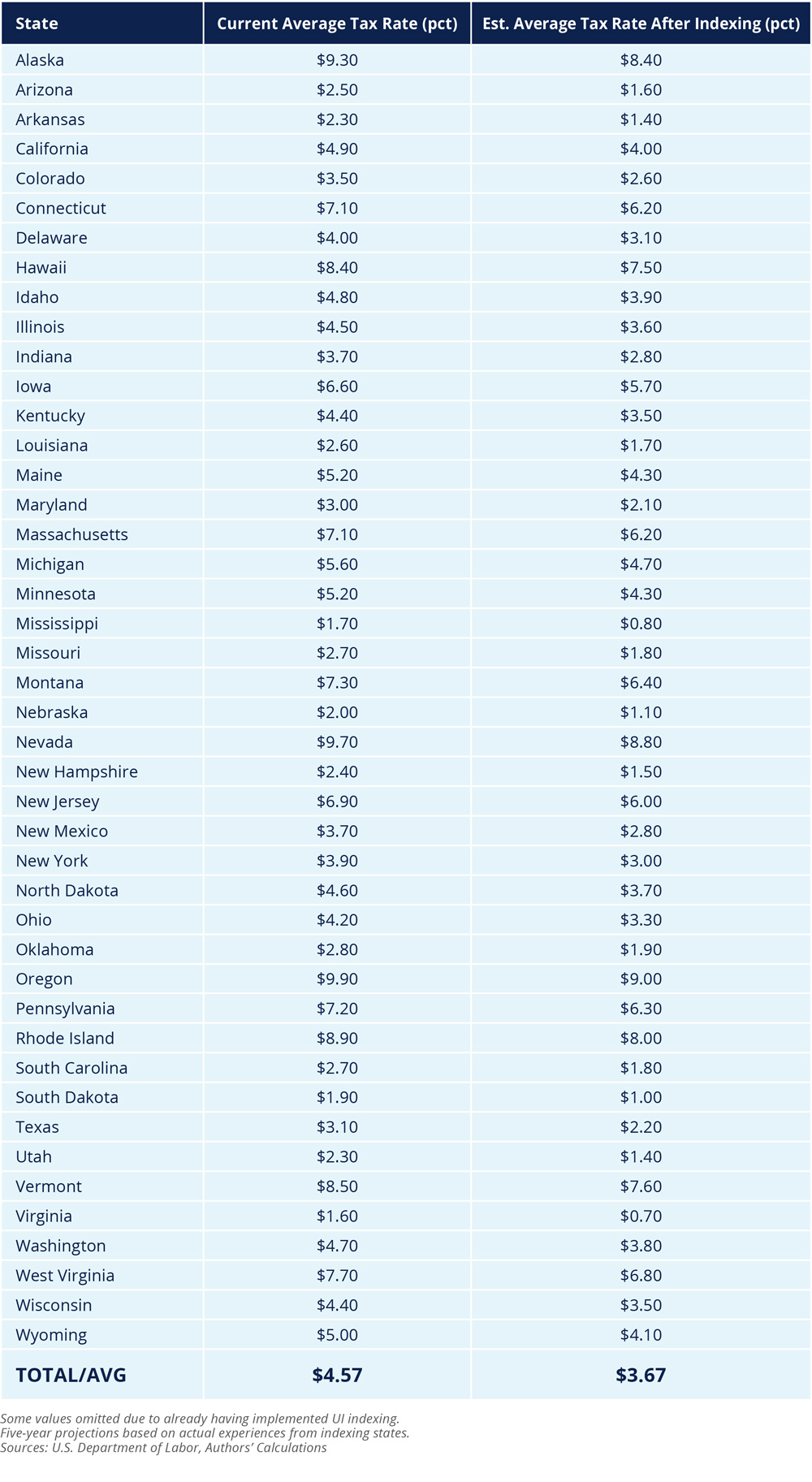

These savings also create room for states to reduce unemployment taxes—and stave off future tax hikes—on small businesses. If states adjusted tax rates to match the increase in program solvency, UI tax rates could be cut by 20 percent on average—without sacrificing solvency at all.38 Some states would have the potential for even larger decreases.39

Indexing unemployment benefits would help turn struggling states into more solvent, more competitive states, whose unemployed workers find jobs faster than ever before.

Bottom line: States should bolster UI trust funds, cut taxes for small businesses, and move the unemployed back to work by indexing UI benefits to economic conditions.

After the Great Recession, some states took important steps to improve their UI systems to prepare for the next downturn. Those steps have paid off, as states that indexed their UI systems to economic conditions have weathered the COVID-19 crisis far better. In both uncertain times and times of normalcy, tying UI to economic conditions is a proven way to boost trust fund solvency, cut unemployment taxes for small businesses, and decrease dependency.

The evidence is clear: Indexing helped states recover from the last economic downturn by getting people back to work sooner. While 26-week states missed the opportunity to be as prepared for the current economic climate as indexing states, implementation is always good policy that would pay off both in times of prosperity and austerity. States should adopt UI indexing to improve their trust fund balances, lower UI tax rates, and improve reemployment in the wake of COVID-19.

Appendix 1: UI Trust Fund Balances Have Declined By 113 Percent Since January 2020

Change in UI trust fund balances between January 2020 and November 2021

Appendix 2: UI Indexing Could Boost Trust Fund Balances by Nearly $39 Billion

Estimated change in UI trust fund balances after indexing

Appendix 3: UI Indexing Could Decrease UI Tax Rates by 20 Percent

Effective employer UI tax rates per $1,000 of wages after indexing

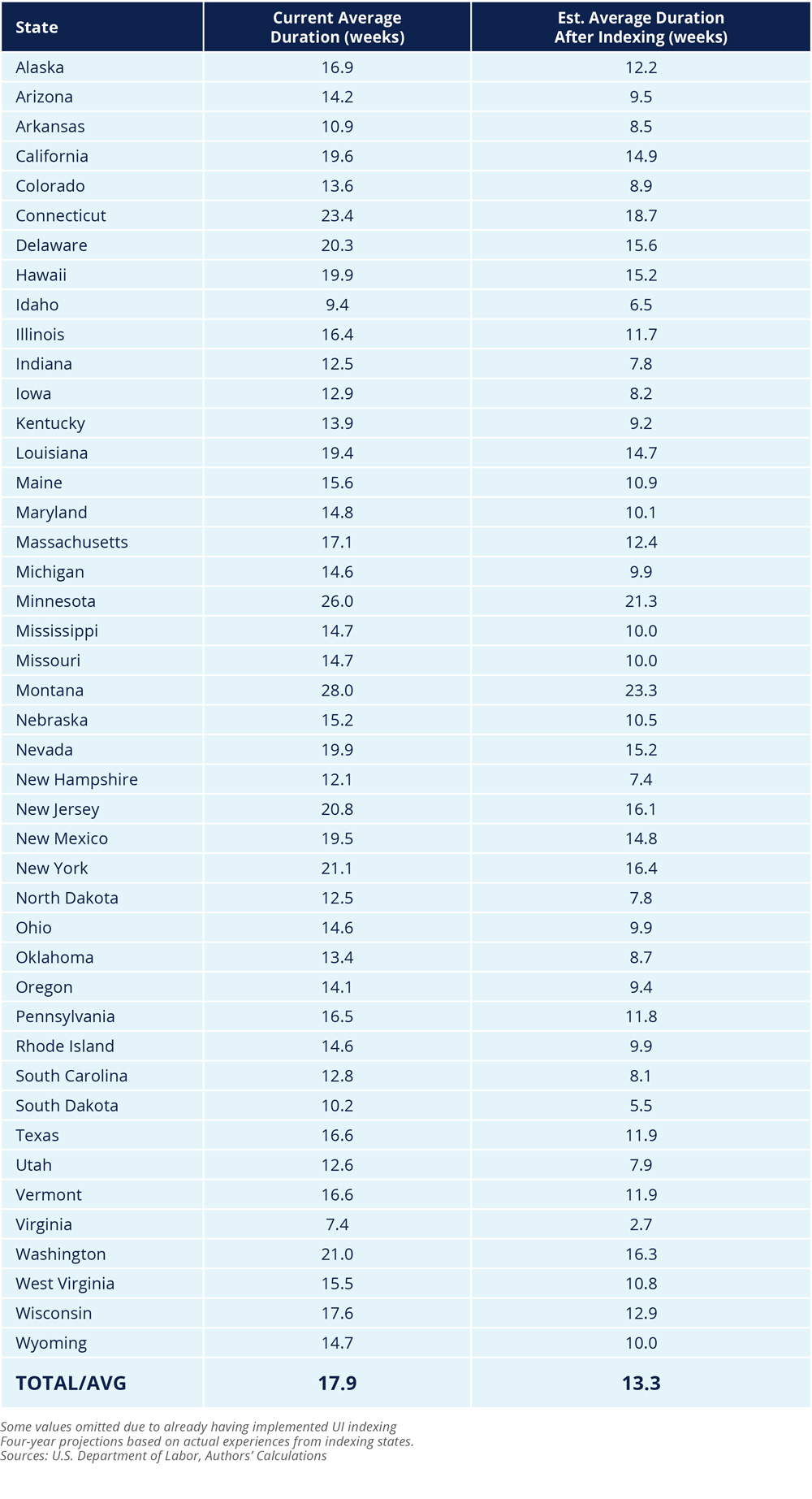

Appendix 4: UI Indexing Could Reduce Average Program Dependency by Nearly 30 Percent

Estimated change in average UI duration after indexing